Closing the Gold Window Opened the Door to Modern Monetary Theory (MMT)

Date Posted: January 22, 2021

Read time: 44 min

This year marks the 50th anniversary of the end of the gold standard in the U.S. In August 1971, President Richard Nixon formally unpegged the U.S. dollar from gold, meaning the greenback was no longer convertible into bullion. Overnight, the dollar became a free-floating currency, measurable only by comparing it to other world currencies.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

This year marks the 50th anniversary of the end of the gold standard in the U.S. In August 1971, President Richard Nixon formally unpegged the U.S. dollar from gold, meaning the greenback was no longer convertible into bullion. Overnight, the dollar became a free-floating currency, measurable only by comparing it to other world currencies.

And yet there were still restrictions on private ownership of gold coins, bars and the like. It wouldn’t be until President Gerald Ford signed a bill in December 1974 that Americans could freely buy and trade bullion, for the first time in over 40 years.

A lot happened as a result. Its price no longer fixed, gold exploded 385% from the end of 1974 to 1980, when the metal topped out at $850 an ounce as the U.S. coped with historical levels of inflation.

Over the past 50 years, gold has expanded more than 46 times, with a compound annual growth rate (CAGR) of about 8%.

The ability to trade gold freely has obviously been good for investors. Today, gold bullion is one of the most liquid assets in the world, its daily volume standing at more than $145 billion, according to the World Gold Council (WGC). Only the S&P 500 and U.S. Treasuries trade more—but not by much.

The Age of Runaway Debt

The drawback is that, in the years since the end of the gold standard, there’s been a significant and growing lack of discipline when it comes to government spending. Before 1971, there was a natural limit to how much money could be printed. New issuances were dependent on the amount of gold sitting in the nation’s coffers.

Today, with the dollar backed not by a hard asset but by the “full faith and credit” of the U.S. government, the federal debt is closing in on an astronomical $28 trillion, which is more than 130% of the size of the U.S. economy.

To give you some idea of how dramatically times have changed, federal debt in 1960 was only a little over half the size of the economy.

The debt is expected to surge even more in the coming months, now that Joe Biden has been sworn in as president and Congressional control has shifted in the Democrats’ favor. Biden, who turned 78 in November, has called for a $1.9 trillion economic relief package that include $1,400 checks for all American adults.

I’m not advocating that we return to the gold standard. It’s probably no longer feasible. According to the Treasury Department, official gold reserves currently stand at approximately 261 million ounces, for a market value of some $493 billion.

That’s just not enough metal to support an economy as large as the U.S.—not unless the price of each ounce of gold was fixed at something outrageous like $100,000.

There’s been some discussion of making Bitcoin a reserve currency. Like gold, its supply is limited, and it has the potential to scale up. But at the moment, cryptos are far too volatile. Both Bitcoin and Ethereum corrected substantially on Thursday (the first 21st day of the 21st year of the 21st century), with the former falling 13%, the latter close to 19%.

So for now, we’re left with the current monetary system of unlimited money-printing, which in turn makes each U.S. dollar less valuable and each ounce of gold more valuable.

The Rise of Modern Monetary Theory (MMT)

What this is all pointing toward is the rapid adoption of modern monetary theory (MMT). I’ve written about the concept before.

In short, proponents of MMT say that governments that issue their own currency, as the U.S. does, are free to spend as much as they want, regardless of the amount of revenue generated. And if the government ends up with a spending deficit, it can just print more money to cover the difference.

Isn’t this what we’re already doing? In 2020, the federal government spent a total of $6.55 trillion, despite it collecting $3.42 trillion—about half of that—in tax revenue.

What’s more, the amount of M1 money supply—which includes the most liquid and readily available forms of money—was up an unprecedented 67% in December 2020 compared to the same month the previous year.

As Ray Dalio, billionaire founder of Bridgewater, the world’s biggest hedge fund, has said a number of times, “Cash is trash.”

Our Favorite Ways to Get Exposure to Gold

So where does Dalio put his money instead? A look at Bridgewater’s third-quarter filings reveals large positions in physical gold and gold mining companies. At 11.6%, the gold-backed SPDR Gold Trust is the fund’s second-largest position. The fifth-largest position, at 3.4%, is the iShares Gold Trust.

Among the gold producers in Dalio’s portfolio are Newmont, Yamana Gold and Freeport-McMoRan.

Besides the securities already mentioned, we also like to get exposure to gold and precious metal miners via the royalty companies.

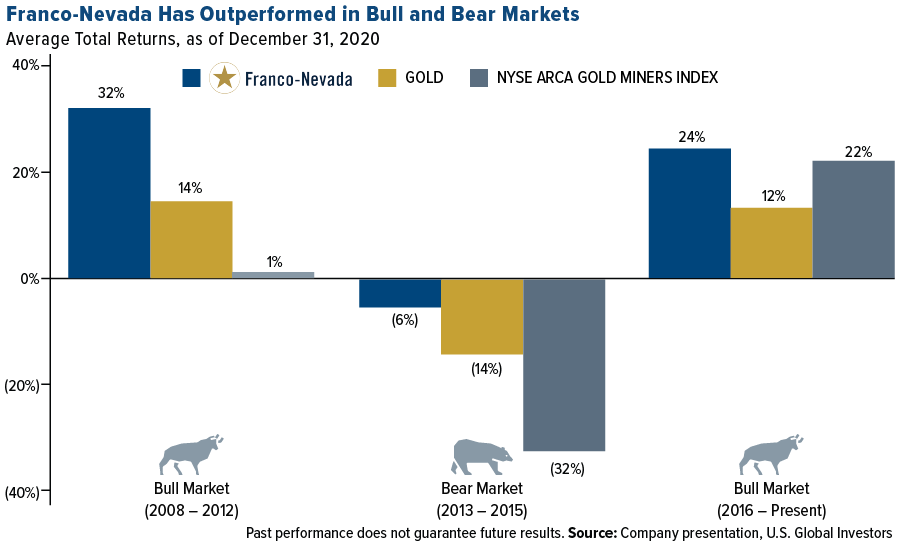

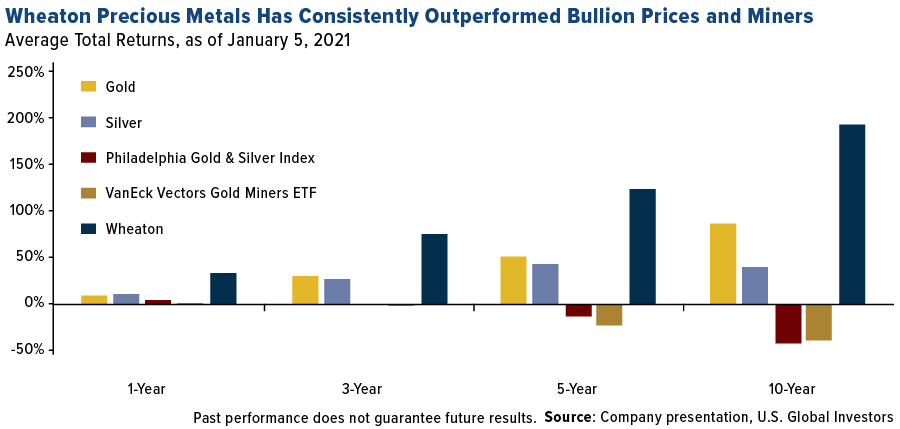

Our two favorites that follow the royalty and streaming model, Franco-Nevada and Wheaton Precious Metals, have impressive track records of outperforming bullion and gold miners over multiple time periods, in bull and bear markets.

Below, you can see that Franco significantly beat gold and senior producers during periods when asset prices were rising as well as falling.

Wheaton similarly performed well over multiple periods. For the one-year, three-year, five-year and 10-year periods, Wheaton crushed not just gold and silver but also miners and the popular VanEck Vectors Gold Miners ETF.

These strong track records have resulted in the companies consistently returning value to shareholders.

As of September 30, Wheaton had an incredible $1.2 billion declared in dividends. Franco, meanwhile, has had 14 straight years of dividend increases, with $1.4 billion paid out since its 2008 initial public offering (IPO).

Both companies are scheduled to report in early March, which I’m eagerly awaiting.

Upcoming GROW Webcast

Speaking of earnings… We’ve already been receiving numerous emails about when to expect the next GROW webcast. There’s now a date in place: February 5 at 7:30am CST. To register for the event, click below.

Gold Market

This week spot gold closed the week at $1,855.61, up $27.16 per ounce, or 1.49%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.78%. The S&P/TSX Venture Index came in strong up 4.34%. The U.S. Trade-Weighted Dollar fell 0.62%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-17 | China Retails Sales YoY | 5.5% | 4.6% | 5.0% |

| Jan-19 | Germany CPI YoY | -0.3% | -0.3% | -0.3% |

| Jan-19 | Germany ZEW Survey Expectation | 59.4 | 61.8 | 55.0 |

| Jan-19 | Germany ZEW Survey Situation | -68.3 | -66.4 | -66.5 |

| Jan-20 | Eurozone CPI Core YoY | 0.2% | 0.2% | 0.2% |

| Jan-21 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jan-21 | Housing Starts | 1560k | 1669k | 1578k |

| Jan-21 | Initial Jobless Claims | 935k | 900k | 926k |

| Jan-26 | Hong Kong Exports | 8.0% | — | 5.6% |

| Jan-26 | Conf. Board Consumer Confidence | 89.1 | — | 88.6 |

| Jan-27 | Durable Good Orders | 1.0% | — | 1.0% |

| Jan-27 | FOMC Rate Deision (Upper Bound) | 0.25% | — | 0.25% |

| Jan-28 | Germany CPI YoY | 0.7% | — | -0.3% |

| Jan-28 | GDP Annualized QoQ | 4.4% | — | 33.4% |

| Jan-28 | Initial Jobless Claims | 875k | — | 900k |

| Jan-28 | New Home Sales | 860k | — | 841k |

Strengths

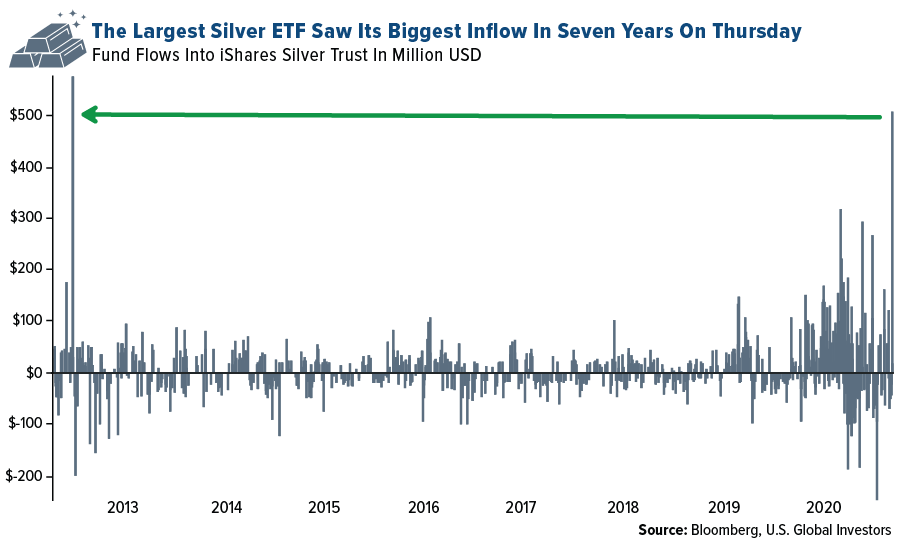

- The best performing precious metal for the week was silver, up 2.92%. Global holdings in silver-backed ETFs hit the highest ever on Wednesday, according to Bloomberg calculations. The iShares Silver Trust took in half a billion dollars in inflows on Tuesday, the biggest inflows in seven years. Despite silver dropping more than 4% so far this year, investors are piling into the precious metal.

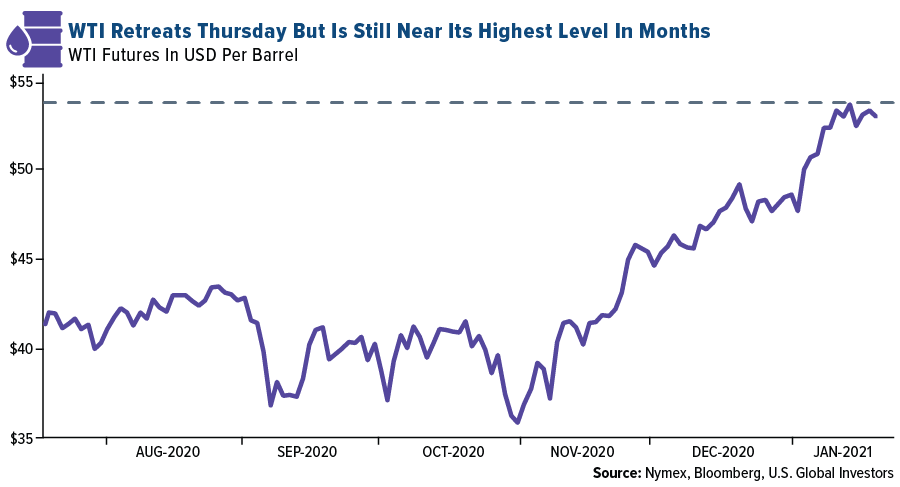

- Spot gold rose 1.7% on Wednesday as Joe Biden was sworn in as the 46th U.S. President. Gold is now trading above last week’s high and is finding support above its 200-day moving average. The dollar weakened amid signs that interest rates may remain low for the near future.

- Anglo Asian Mining shares rose 10% in U.K. trading on Thursday on the news of a ceasefire agreement in Azerbaijan. There had been a military conflict between Armenia, Azerbaijan and Russia over the enclave of Nagorno Karabakh, where Anglo Asian has three contract areas.

Weaknesses

- The worst performing precious metal for the week was palladium, down 1.21% on little market-moving news. Gold and silver were both down sharply Friday morning after U.S. PMI flash readings came in stronger than expected, signaling a strengthening economy.

- GlobalData estimates global gold production final figures will show a drop of 5.4% in 2020 to 108 million ounces, largely due to pandemic disruptions. The biggest decline is expected out of China of 933,800 ounces lower than 2019.

- An explosion at a Chinese gold mine on January 10 trapped 22 workers and has killed one, reports Xinhua News. Workers remain trapped in the Hushan Gold Mine in Shandong province and the rescue team warned their efforts face several challenges due to the hard rock.

Opportunities

- Sibanye Stillwater’s CEO and well-known dealmaker Neal Froneman said he wants to double the size of the South African miner before retiring in two to three years. Froneman grew Sibanye to a market cap of $11.9 billion through mine acquisitions. “M&A is what we are good at. We have created value and we are going to continue to create value in the right way at the right time.” The company is exploring deals in battery metals projects.

- Eldorado Gold and QMX Gold Corporation announced a friendly acquisition. Eldorado, which owns 17% of QMX, will acquire all remaining outstanding shares of QMX at a 39.5% premium. Following the completion of the agreement, QMX shareholders will own 2.8% of the issued and outstand shares of Eldorado.

- Gold Fields has hired former Anglo American Platinum chief Chris Griffith as its new CEO as the company hopes to restore its last gold mine in South Africa, the iconic and challenging South Deep mine. Gold Fields shares rose as much as 6.2% in South African trading on the news. Griffith who left Anglo American Platinum on a high point for the company last year will start in April at Gold Fields.

Threats

- Billionaire investor and Oaktree Capital Management cofounder Howard Marks questioned gold’s worth in a CNBC interview this week. Marks said “gold’s value is almost like a superstition” since it depends on people believing it’s worth something.

- Georgette Boele, senior precious metals strategist at ABN AMRO, adjusted her outlook for gold and said its price has peaked. Boele predicts the gold market struggling this year as rising inflation could force the Federal Reserve to tighten monetary policy faster than expected. Improving economic conditions will push nominal yields higher, which would raise real interest rates, Boele added.

- British Prime Minister Boris Johnson said on Thursday it is still too early to say when the national COVID lockdown in England will end as deaths from the virus keep rising. The U.S. hit a grim milestone of 400,000 COVID deaths this week. Newly sworn in President Joe Biden said another 100,000 Americans could die over the next month as the pandemic will worsen before it improves.

Index Summary

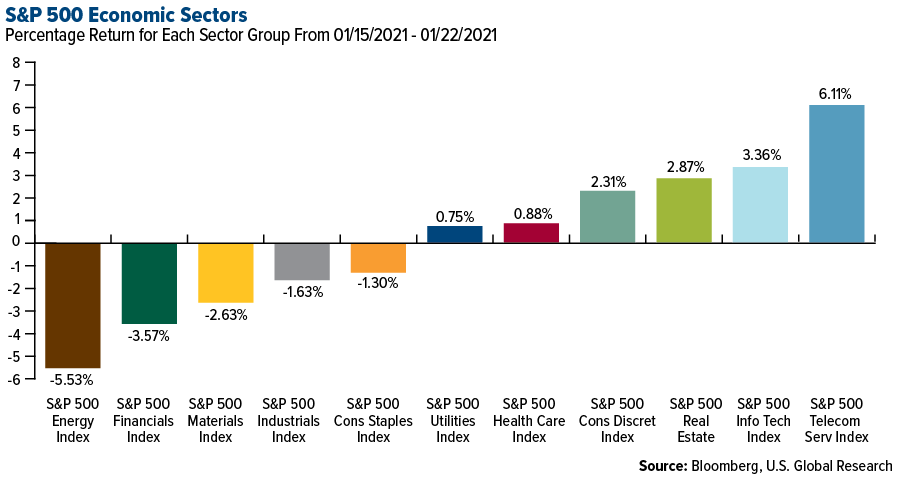

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.59%. The S&P 500 Stock Index rose 1.94%, while the Nasdaq Composite climbed 4.19%. The Russell 2000 small capitalization index gained 2.15% this week.

- The Hang Seng Composite rose 4.59% this week; while Taiwan was up 2.58% and the KOSPI rose 1.77%.

- The 10-year Treasury bond yield remained essentially flat at 1.085%.

Domestic Economy and Equities

Strengths

- U.S. manufacturing activity surged to its highest level in more than 13 years in early January amid strong growth in new orders. IHS Markit said its flash U.S. manufacturing PMI accelerated to a reading of 59.1 in the first half of this month, the highest since May 2007, and up from 57.1 in December. Economists had forecast the index slipping to 56.5 in early January.

- Homebuilding and permits surged in December as historically low mortgage rates supported the housing market. Housing starts jumped 5.8% to a seasonally adjusted annual rate of 1.67 million units last month, the Commerce Department said on Thursday. Economists polled by Reuters had forecast starts would rise to a rate of 1.56 million units in December.

- PulteGroup Inc was the best performing S&P 500 stock for the week, increasing 15.25%. Janney Montgomery Scott analyst Tyler Batory initiated coverage of the company with a buy rating. The analyst favors builders with move up and balanced buyer exposure such as PulteGroup over the “entry-level heavy builders” such as D.R. Horton and Meritage Homes.

Weaknesses

- Around 900,000 Americans filed for initial jobless claims last week, versus economists’ projections of 925,000, according to the first labor market data released under President Joe Biden. First-time weekly jobless claims, a proxy for layoffs, have exceeded 750,000 each week since summer, and surged to a revised 926,000 for the week ended January 9 as rising coronavirus cases continue to keep consumers home and businesses under restrictive measures.

- The pandemic took a fresh toll on the holiday shopping season, with sales at retail stores falling for three months in a row. Sales at restaurants and bars tumbled 4.5% in December and collapsed by one-fifth for 2020 as a whole.

- Nov Inc was the worst performing S&P 500 stock for the week, decreasing 13.87%. BMO Capital Markets lowered their 2020-22 estimates for Nov following its 4Q20 pre-announcement in which revenues were slightly lower.

Opportunities

- The main event next week will be the Fed meeting on Wednesday. There isn’t any scope for policy changes, so any market reaction will come down to Chairman Powell’s comments. Powell and other senior Fed officials have recently pushed back on the idea that a stronger economic outlook implies the Fed may begin to decrease its QE dose soon, and he will likely reaffirm that message.

- Walt Disney Co. shares jumped higher Friday after analysts at UBS boosted their price target on the entertainment group, citing improved prospects for its parks division and the scale-up of its Disney+ streaming service. UBS analyst John Hodulik improved his rating on the stock to ‘buy" from ‘neutral, while boosting his price target by $45 to $200 per share, citing the group’s potential to challenge Netflix’s streaming dominance and reach 340 million global subscribers for its Disney+ service by 2024.

- Apple is preparing its first AR headset. Bloomberg’s Mark Gurman reported the device is expected to be a niche product, and a precursor to a more advanced device down the line.

Threats

- Negotiations begin next week between Democrats and Republicans on Biden’s $1.9 trillion proposal for a stimulus relief package. Signs that the size of the package may need to be reduced substantially in order to get bipartisan support would be negative for market sentiment.

- International Business Machines Corp. shares fell the most in 10 months after the company reported a greater sales decline in the fourth quarter than analysts had expected, signaling CEO Arvind Krishna’s turnaround plan may take more time. Sales fell 6.5% to $20.4 billion in the three months ended December 31.

- Warren Buffett’s right-hand man flagged a "speculative frenzy" in the stock market and signaled that he doesn’t expect share prices to climb much higher. Charlie Munger, the vice chairman of Buffett’s Berkshire Hathaway conglomerate, is also the chairman of Daily Journal Corporation, a newspaper publisher and software developer. Daily Journal’s stock price hit a record high of $404 on December 31. It had surged by roughly 50% in the previous four weeks. "This price was reached amid much speculative frenzy and much forced buying by index funds," Munger said in his letter to Daily Journal shareholders this month. The 97-year-old investor also touched on Daily Journal’s stock portfolio, which counts Bank of America and Wells Fargo among its holdings. Its value soared by 45%, to $260 million, in the fourth quarter of 2020. "Shareholders should not expect any significant appreciation above that level anytime soon," he said.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 20.08%, with the last two trading sessions of the week capped by limit-up barriers. Lumber prices had fallen precipitously since the start of the year but now have sharply rebounded. On his first day in office, President Joe Biden took steps for America to rejoin the Paris Climate Accord, reversing Trump’s decision to pull out from the agreement. This is a major step in pushing the U.S. toward clean energy and is positive for renewable energy producers and those involved in the production of metals and minerals used.

- HysetCo., a venture part-owned by Toyota Motor Corp and Air Liquide SA, has raised $97 million to help hasten the shift of the Paris taxi force to hydrogen-powered cars by 2024, when the city hosts the Olympic Games. The group has already used funds to replace diesel taxis. Bloomberg notes that while many carmakers are now spending vast sums to develop battery vehicles, Toyota is one of just a few to invest heavily in hydrogen-powered cars, which remain more costly to produce.

- China’s National Energy Administration said in a press release on Wednesday that China added almost 72 gigawatts of wind power in 2020, more than double the previous record. The country also added about 48 gigawatts of solar, the most since 2017, and about 13 gigawatts of hydropower.

Weaknesses

- The worst performing commodity for the week was natural gas, down 10.67%. U.S. natural gas futures had the biggest weekly loss since November amid outlooks for warmer temperatures in the South and Mideast, cutting into demand for the heating fuel.

- Iron ore had big price swings this week as major suppliers boosted forecasts for output. Both BHP Group and Rio Tinto Group increased forecasts and data showed a pick-up in cargos out of Australia, Bloomberg reports.

- The International Energy Agency (IEA) has again lowered its forecast for oil demand in the first quarter to just 600,000 barrels a day as renewed lockdowns temper the expected recovery. The world’s swollen inventories should decrease by 100 million barrels in the next three months as Saudi Arabia and other OPEC+ producers cut production, reports Bloomberg. Schlumberger said it sees oil demand rising back to pre-virus levels by 2023.

Opportunities

- The United Arab Emirates aims to become a blue hydrogen powerhouse to help cut carbon emissions by nearly a quarter. The country will use carbon-capture technologies to create

what’s known as blue hydrogen, supplying cleaner energy, Sultan Al Jaber, CEO of Abu Dhabi National Oil Co. and UAE Industry Minister, said at a virtual conference on Tuesday. - Alrosa PJSC expects the diamond market to continue recovering after record sales in December allowed it to raise prices, reports Bloomberg. The Russian diamond giant said strong sales of $521.6 million last month underlined a strong demand recovery in key U.S. and Chinese markets.

- Suzano SA, the world’s largest wood pulp maker said a sharp recovery in prices should benefit earnings and speed up de-leveraging in the first quarter. Bloomberg notes global supplies of the material used to make paper cups, tissue and cardboard are tightening as Chinese demand bounces and producers cut output. Suzano recently raised prices in China to change $580 a metric ton for hardwood pulp starting in February.

Threats

- A Bloomberg Businessweek story this week commented how the U.S. is not only losing the battery race, but it’s barely in the running. BloombergNEF estimates America’s share of global battery production will fall from 8% today to 6% in 2025. Although there are a few battery factories planned in the U.S., China currently dominates the market by far and Europe is taking big steps to expand its domestic production. “If we want to have a domestic supply chain for batteries in North America, now is the time you have to press the accelerator,” said Sam Jaffe, managing director of Cairn Energy Research Advisors. “The conversation should be ‘mine to car,’ not just ‘battery to car.’

- American exploration and production stocks plunged after the Interior Department halted issuing oil and gas leases for 60 days that affects all federal lands, minerals and waters. This is a strong reversal from the Trump administration’s relaxed environmental policies. Although positive for the environment, the Biden administration is a big threat to traditional energy producers and explorers.

- Saudi Aramco promised investors climate friendliness and transparent reporting. But the oil giant’s accounting for its greenhouse gas fails to provide a complete picture, reports Bloomberg. The Saudi oil giant excludes emissions generated from many of its refineries and petrochemical plants in its overall carbon disclosures, according to a review of public filings by Bloomberg Green. This is a red flag for investors who are keen on accounting for emissions risk in their portfolios.

Airline Sector

Strengths

- The best performing airline stock for the week was TUI AG, up 9.7%. Delta indicated that it would receive $2.9 billion from the Treasury as part of the payroll support program. Nearly $2 billion of this is for grants, and $830 million is an unsecured 10-year loan. Nearly $1.4 billion of this was received on January 15. American Airlines is slated to receive $3 billion, with $1.5 billion being received on January 15. JetBlue has received $252 million from the U.S. Treasury.

- EasyJet is indicating that summer holiday bookings in Europe are surging. Bookings are up 250% year-over-year, and May is the most active month for reservations. Leisure carriers are leading business carriers in the early stage of this travel recovery.

- Chinese airlines continue to dominate airline rankings, paralleling the country’s relatively early recovery from the COVID-19 pandemic. Nine of the top 20 airlines ranked by departures are Chinese airlines. However, the government has just mandated pre-flight COVID testing for passengers, which curtailed demand.

Weaknesses

- The worst performing airline stock for the week was GOL, down 8.9%. Wizz Air indicated that its traffic will be down 70% in the second quarter ending March 31. Only 30% of its fleet is operational due to virus-related lockdowns and travel restrictions. Recovery is expected in fiscal year 2022, but revenues at best may be only 85% of pre-pandemic highs. The U.K. government recently announced that all travel corridors would close, which could push this forecast out in time.

- IAG (who owns British Airways and Iberia) amended its original agreement to buy Air Europa for 1 billion Euros. IAG reduced the purchase price to 500 million Euros. The payment is being delayed until six years after the deal is completed in the second half of 2021.

- United Airlines lost $1.9 billion in the fourth quarter of 2020. This was lower than analyst estimates. The company lost $7.1 billion in 2020, and the carrier burned though $33 million of cash per day. Revenues were down 70%, and the airline indicated this would continue in the first quarter of 2021.

Opportunities

- Governments continue to support the airline industry. The Biden administration is considering setting up an Airline Recovery Commission. This group will focus on the industry’s recovery from the pandemic, and will include government officials, industry executives, labor unions and science/health advisors. Norway also indicated that it is willing to keep Norwegian Air afloat by giving a loan to the airline with many undefined conditions attached.

- United Airlines indicated that profit margins may top pre-pandemic levels by 2023. EBITDA margins in 2023 should be higher than 2019. The company has $19.7 billion in liquidity and has recently cut costs by $1.4 billion. An additional $2 billion of cost cuts could start soon.

- Airline industry traffic data is pointing to a recovery, albeit slow. Even though traffic was down 64% year-over-year, traffic was up 5% from the prior week. Airlines are slowly increasing routes. Singapore Airlines indicated that it wants to restart passenger flights to Munich. Qatar Airways plans to increase service to U.S. cities.

Threats

- There were two lawsuits from various environmental groups that indicated that recent carbon emission standards for planes do not go far enough in reducing greenhouse gases. They indicate that these standards are 10 years behind their time. The airline industry represents about 12% of the carbon-based pollution in the U.S.

- KLM indicated that it is no longer able to fly long distance routes due to stricter travel rules. International flights are hampered by the requirement to have a rapid COVID test for passengers. The company also reduced staff by 1,000 related to this move.

- Most European airlines are continuing to suffer from weak traffic. Slow vaccine rollouts and a delayed recovery are concerning many airline managements in Europe, particularly that there may be a summer holiday season far below expectations. Traffic drops are exacerbated by different standards among the countries in Europe, and the lack of knowledge by passengers about these standards. The table below indicates how sharply the traffic drop has been not only in Europe, but all over the world.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 1.3%. The best performing country in Asia this week was Taiwan, gaining 2.6 basis points.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 1.7%. The Taiwanese dollar was the best performing currency in Asia this week, gaining 35 basis points.

- Taiwan export orders rose by 38% year-over-year in December, most since 2010 supported by strong demand for chips and technical products and parts. The global chip crunch will likely further boost Taiwan’s key role in the technology supply chain.

Weaknesses

- The worst performing country in emerging Europe for the week was the Czech Republic, losing 2.3%. The worst performing country in Asia this week was the Philippines, losing 2.7%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 2.1%. The Indonesia rupiah was the worst performing currency in Asia this week, losing 60 basis points.

- Inflation in Europe is very low. The final December CPI was reported at negative 30 basis points, well below the central bank’s target “but closer to 2 percent”. Eurozone’s core inflation is slightly higher at positive 20 basis points. Greece has the lowest inflation among the 27 members of the eurozone, which stands at negative 2.3 percent.

Opportunities

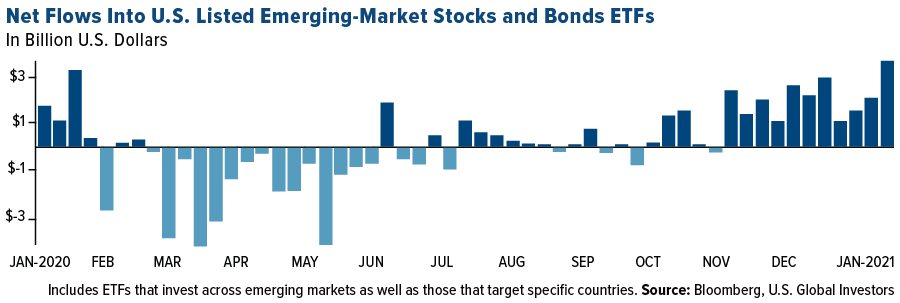

- Investors added $3.6 billion to exchange-traded funds that buy emerging markets stocks and bonds in the week ended January 15. This was the 11th straight week of inflows, supported by a weaker dollar and President Biden’s victory in the United States. Larger stimulus is expected which should result in faster growth for developing nations.

- The Chinese electric vehicle sector is growing, with China-based manufacturers accounting for over 50 percent of global electric vehicle deliveries. Due to a global push toward green energy the global demand for EV cars, is likely to increase, and demand for EVs in China is likely to remain strong as the Chinese government wants about 25 percent of all new cars sold in the country to be electric by 2025, up from roughly 5 percent at present.

- According to Ed Hyman’s research from Evercore ISI, the coronavirus cases have started to fall in the Unites States, United Kingdom and Canada suggesting that we have passed the peak of infections that spiked after the holidays. Odds are probably up to 55 percent that cases have indeed peaked.

Threats

- Alexy Novalny, Putin’s biggest critic, was arrested in Moscow upon his arrived from Germany where he was recovering from Novichok poisoning. On Tuesday, he released a video accusing Vladimir Putin of corruption. Novalny’s supporters are planning mass protests this weekend demanding his release.

- Due to a spike in coronavirus cases in China, the government, and companies there are paying people not to travel for family reunions and sightseeing during the Lunar New Year holiday. They are offering money, shopping vouchers, movie tickets and other incentives to stay in cities and at home. The 16-day celebration is usually full of activities that stimulate the country’s growth, but this year may be different.

- European Central Bank (ECB) President Christine Lagarde signaled that the eurozone economy is headed for a double-dip recession, saying that the current level of monetary stimulus is not enough. The bank’s rates were unchanged and mostly will remain unchanged or move lower until inflation improves. More action from the ECB may take place in March when new economic forecast will be available and a clearer view of how the crisis will develop is made.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Enjin Coin, rising 110.26%.

- Two hospitals in England are using blockchain to keep records of storage and supply of temperature-sensitive COVID-19 vaccines. Everyware, a digital asset tracking and monitoring provider, and Hedera Hashgraph, an enterprise-grade distributed ledger provider, are the companies spearheading the initiative for an initial group of National Health Service hospitals within the Stratford Upon Avon and Warwick system. Texas-based Hedera Hashgraph is owned by Google and IBM.

- Microsoft and Tanla Platforms, an India-based cloud communications firm, launched a blockchain-based communications platform aimed to offer more private and secure messaging. Wisely, the communications platform is mainly being targeted at enterprises, mobile carriers, and over-the-top content providers. Wisely has been granted three patents in cryptography and blockchain processes by the U.S. Patents & Trademark Office and will be sold by both Microsoft and Tanla Platforms, globally.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was IOST, down 24.05%.

- Bitcoin and Ethereum have started slipping down from their all-time highs posted just within the last two weeks. Even as equities and indexes were showing positive signs before and after President Biden’s inauguration and the increased possibility of another stimulus bill, cryptocurrencies turned bearish for the short-term. From their record highs, Bitcoin has dropped by 22.32% in two weeks and Ethereum has dropped by 13.66% in just three days, fueling the imminent criticism of the asset class’ short-term volatility.

click to enlarge

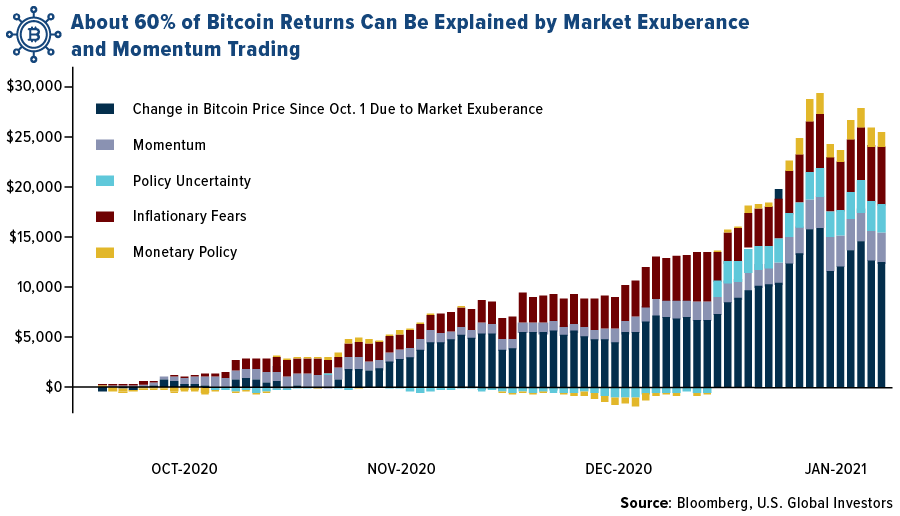

- Strategists at JPMorgan are questioning Bitcoin’s utility as a reliable investment hedge as the cryptocurrency’s mainstream usage seems to be reducing its diversification benefits. The memo published by the strategists also suggests that Bitcoin has recently heightened correlation with traditional markets, reaching an all-time high correlation of 0.23 with the S&P 500 over 180 days. The chart shows that about 60% of Bitcoin’s returns since October 2020 are a result of market exuberance and momentum trading, which could explain the recent decline in the cryptocurrency’s price as investor confidence decreases in the short-term and the asset is perceived to be a bubble.

Opportunities

- BlackRock’s latest SEC filing indicates that the asset manager is preparing to enter the Bitcoin derivatives market through two of its funds – BlackRock Funds V and BlackRock Global Allocation Fund. This filing comes a month after the asset manager reported that it is looking for a Blockchain VP to implement strategies specifically designed to drive demand for the firm’s offerings within the cryptocurrency space. Janet Yellen, Biden’s treasury secretary nominee, wrote to the Senate Finance Committee that it is important for the U.S. to consider the benefits of cryptocurrencies while of course still being wary of their potential for misuse. She believes that the U.S. needs to look closely at how to encourage their use for legitimate activities and how to implement an effective regulatory framework for the cryptocurrencies and other fintech innovators.

- VanEck, a major investment management firm, is making another attempt to launch a digital asset ETF. According to its SEC filing, the Digital Asset ETF will invest in companies that operate digital asset exchanges, payment gateways, mining operations, software, equipment and technology or services to the digital asset industry.

- Grayscale Investments looks to be preparing for possible launches of five new single-asset trusts for cryptocurrencies. The world’s largest digital asset manager filed trusts with Delaware’s corporation’s registry for Chainlink, Basic Attention Token, Decentraland, Livepeer and Tezos. Grayscale mentioned that the company is always looking for opportunities to offer products to meet investor demands but a filing does not necessarily mean that a product is going to launch in the market.

Threats

- Guggenheim Partners’ CIO, Scott Minerd, is expecting Bitcoin to have a price pullback after its rally to approximately $42,000. Minerd believes that the price of the cryptocurrency will fall to $20,000 just a month after saying that the fair value of Bitcoin should be $400,000.

- President Biden’s nominee for Treasury Secretary, Janet Yellen, said this week that lawmakers should curtail the use of cryptocurrencies over concerns that the assets are being used for illegal activities. She added that majority of the transactions taking place within the cryptocurrency world are for illicit financing and that lawmakers need to examine ways in which they can ensure that money laundering does not occur through these untraceable channels.

- Eight minority Ethereum mining pools, amounting to approximately 30% of the network’s hash power, have threatened to form a cartel of sorts to push back against the implementation of Ethereum Improvement Proposal (EIP) 1559, which they say unfairly cuts into their bottom line as it burns most of the transaction fees typically given to miners in order to reduce the transaction fee volatility and improve the blockchain’s woeful UI. The small pool is calling on Ethereum miners to essentially boycott major mining pools that support EIP 1559 such as Sparkpool and F2Pool.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.09 | +0.00 | +0.09% |

| Oil Futures | 52.07 | -0.29 | -0.55% |

| Hang Seng Composite Index | 4,723.89 | +207.36 | +4.59% |

| S&P Basic Materials | 468.43 | -5.61 | -1.18% |

| Korean KOSPI Index | 3,140.63 | +54.73 | +1.77% |

| S&P Energy | 317.54 | -5.04 | -1.56% |

| Nasdaq | 13,543.06 | +544.56 | +4.19% |

| DJIA | 30,996.98 | +182.72 | +0.59% |

| Russell 2000 | 2,168.76 | +45.56 | +2.15% |

| S&P 500 | 3,841.47 | +73.22 | +1.94% |

| Gold Futures | 1,856.70 | +23.00 | +1.25% |

| XAU | 140.15 | +2.64 | +1.92% |

| S&P/TSX VENTURE COMP IDX | 945.68 | +37.68 | +4.15% |

| S&P/TSX Global Gold Index | 311.07 | +4.27 | +1.39% |

| Natural Gas Futures | 2.45 | -0.29 | -10.41% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,140.63 | +380.81 | +13.80% |

| 10-Yr Treasury Bond | 1.09 | +0.14 | +14.81% |

| Gold Futures | 1,856.70 | -25.60 | -1.36% |

| S&P Basic Materials | 468.43 | +20.55 | +4.59% |

| S&P 500 | 3,841.47 | +151.46 | +4.10% |

| DJIA | 30,996.98 | +867.15 | +2.88% |

| Nasdaq | 13,543.06 | +771.95 | +6.04% |

| Oil Futures | 52.07 | +3.95 | +8.21% |

| Hang Seng Composite Index | 4,723.89 | +549.60 | +13.17% |

| S&P/TSX Global Gold Index | 311.07 | -8.81 | -2.75% |

| XAU | 140.15 | -2.86 | -2.00% |

| Russell 2000 | 2,168.76 | +161.65 | +8.05% |

| S&P Energy | 317.54 | +28.34 | +9.80% |

| S&P/TSX VENTURE COMP IDX | 945.68 | +103.79 | +12.33% |

| Natural Gas Futures | 2.45 | -0.16 | -5.98% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 140.15 | -6.26 | -4.28% |

| S&P/TSX Global Gold Index | 311.07 | -44.27 | -12.46% |

| Gold Futures | 1,856.70 | -61.10 | -3.19% |

| DJIA | 30,996.98 | +2,633.32 | +9.28% |

| S&P 500 | 3,841.47 | +387.98 | +11.23% |

| Nasdaq | 13,543.06 | +2,037.05 | +17.70% |

| Korean KOSPI Index | 3,140.63 | +812.74 | +34.91% |

| Natural Gas Futures | 2.45 | -0.56 | -18.46% |

| S&P Basic Materials | 468.43 | +55.29 | +13.38% |

| Russell 2000 | 2,168.76 | +538.50 | +33.03% |

| Oil Futures | 52.07 | +11.43 | +28.13% |

| Hang Seng Composite Index | 4,723.89 | +820.86 | +21.03% |

| S&P/TSX VENTURE COMP IDX | 945.68 | +228.89 | +31.93% |

| S&P Energy | 317.54 | +86.30 | +37.32% |

| 10-Yr Treasury Bond | 1.09 | +0.23 | +26.60% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

Delta Airlines

JetBlue Airways

American Airlines

Wizz Air Holdings

Qatar Airways

Air Liquide SA

BHP Group Ltd

Schlumberger NV

Gold Fields Ltd

Anglo American PLC

Sibanye Stillwater Ltd

Eldorado Gold Corp

Newmont Corp

Franco-Nevada Corp

Wheaton Precious Metals Corp

SPDR Gold Shares

Apple Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

M1 Money Supply includes funds that are readily accessible for spending.

The Philadelphia Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.